Note: This section is so chock full of tables & graphs that I've broken it into two sub-sections...I'll be posting the 2nd half of Part 5 over the weekend...

If you've ever wondered why healthcare wonks (myself included) rarely talk about the ACA's Catastrophic Level plans (or at least it was rare up until last year, when the Trump Regime decided to try opening up the floodgates on them), and why the only time I usually discuss Platinum Plans is in the context of high-CSR enrollees being eligible for "Secret Platinum" plans (labeled as Silver), the first table below should explain why.

Catastrophic ACA plans are only available at all in 34 states +DC (this is actually down from 40 states +DC last year), and less than 0.3% of all ACA exchange enrollees choose Catastrophic plans...just 67,000 nationally. Even if you only include the states where they're available this only increases to 0.36% (although they did reach 4.4% of total enrollments in Montana this year).

Note: This is mostly an updated version of a post of mine from last May, when it looked as though Senate Republicans were going to include "funding CSR reimbursement payments" as part of their Big Ugly Bill (officially the "One Big Beautiful Bill Act") which, among many other terrible things, included gutting Medicaid and didn't include extending the ACA's enhanced premium tax credits beyond December 2025.

Thankfully, in the end the Senate GOP didn't include the CSR funding provision...but House Republicans did include it in a bill which they passed last winter...which then died in the Senate since it would have required 60 votes there to move forward.

Next up: Age brackets, gender, racial/ethnic groups and urban/rural communities. I'm also throwing in the stand-alone Dental Plan table here for the heck of it since I don't know where else to include it.

Nationally, there hasn't been that much of a shift in the enrollment breakout by age bracket...but within each bracket there's a couple of takeaways:

As expected given the subsidy expiration, enrollment among young adults plummeted (down 7.4% & 8.5% among 18-25 yr olds & 26 - 34 yr olds respectively). This will absolutely have a disproportionate negative impact on the risk pool (and, thus, gross premiums) next year

On the other hand, enrollment of children actually increased by 3.4% year over year, which I wasn't expecting at all.

I was also surprised to see that enrollment among seniors inched up ever so slightly (about 0.4%, or 1,500 people). Huh.

Next up: Premiums, Advance Premium Tax Credits (APTC) and Cost Sharing Reduction (CSR) assistance.

Nationally, the average unsubsidized premiums for 2026 exchange-based Open Enrollment Period enrollees are $741/month, up $122/month or 19.7% from last year.

This is a smaller average gross increase than the 25.5% I had projected last fall...for two rather obvious reasons, which I try to make clear every year:

Now it's time to move on to the actual demographic breakout of 2026 Open Enrollment Period (OEP) Qualified Health Plan (QHP) enrollment.

First up: Breaking out new enrollees vs. existing enrollees who either actively re-enroll in an exchange plan for another year or who passively allow themselves to be automatically renewed into their current plan (or to be "mapped" to a similar plan if the current one is no longer available).

Nationally, 15.6% of all exchange QHP enrollees were new this year. The other 84.4% are current enrollees who signed up for another year.

Fortunately, more enrollees took my advice and actively re-enrolled this year (46.3% vs just 39% last year). Unfortunately, 38.1% still allowed themselves to be passively auto-renewed. Those are the ones who, in many cases, were likely hit with massive sticker shock as they were auto-renewed into a plan which probably had dramatically higher premiums due to the enhanced tax credits expiring...over 8.8 million enrollees nationally.

When I last checked in on the official 2026 ACA Open Enrollment Period (OEP) data from the Centers for Medicare & Medicaid Services (CMS), they had published the "top line" enrollment numbers for each state, including final numbers for the 30 states hosted via the federal ACA exchange (HealthCare.Gov) and semi-final data for the remaining 20 states (+DC) which operate their own ACA exchanges.

I've repeatedly warned that the final, official CMS 2026 OEP report--which includes far more detailed demographic data including breakouts by metal level, income brackets, financial assistance and so forth likely wouldn't be published until late April or early May based on last year when it wasn't published until May 11th.

Well, it turns out they moved that up substantially after all: The final 2026 OEP Public Use File was just uploaded at CMS today...and while there hasn't been any formal press release published yet, I have a copy regardless.

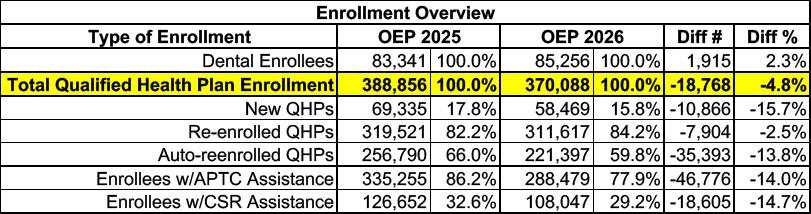

Here's the overview of Virginia ACA exchange enrollment over the course of OEP 2026 vs. 2025. Stand-alone dental plan enrollment is up 2.3%, which is nice, but overall major medical plan (Qualified Health Plan, or QHP) enrollment dropped by nearly 19,000 people, or 4.8% year over year.

There's also 14% fewer enrollees receiving federal tax credits than last year (nearly 47,000 people), while another 15% lost Cost Sharing Reduction assistance (CSR).

Last month I posted a massive3-partseries of articles which looked at nearly 3 dozen changes being proposed by the Trump Regime's Centers for Medicare & Medicaid Services (CMS) to how the Affordable Care Act will be administered starting this fall (for the 2027 plan year).

The changes ranged from the mundane (for instance, one provision simply says that the per enrollee user fees paid by insurance carriers to HHS to pay for HealthCare.Gov's operations will remain the same as they are this year) to the devastating (up to 1.5 million legally-present immigrants who were previously eligible for ACA tax credits, including victims of domestic abuse and human trafficking, either already are or will soon become ineligible for financial assistance).