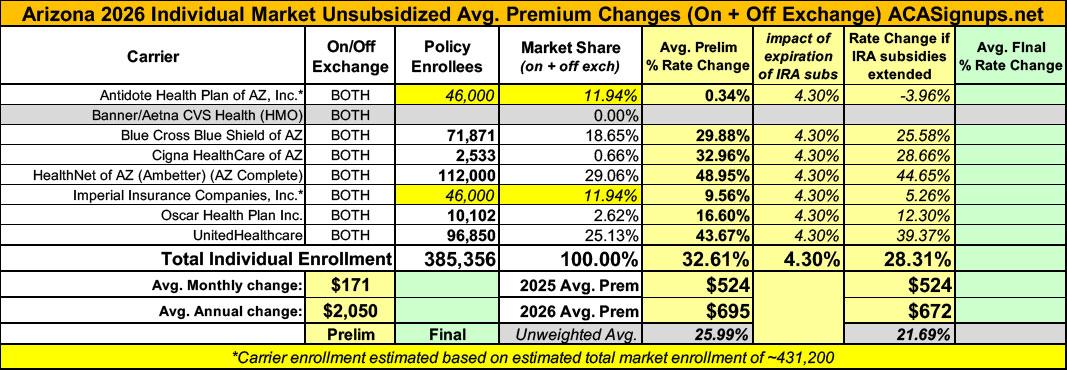

2026 Rate Changes - Arizona: +32.6%; ~430,000 enrollees facing MASSIVE rate hikes starting in January

Thu, 08/07/2025 - 12:12pm

Overall preliminary rate changes via federal Rate Review database.

Antidote Health Plan of AZ:

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Banner/Aetna CVS:

(Dropping out of the individual market for 2026.)

Blue Cross Blue Shield of AZ:

BCBSAZ is filing an average rate increase for plans in the Arizona Individual market of 29.88%, varying between 14.7% and 38.6%, excluding federally prescribed age factors. The average increase is calculated from the most recently implemented rates which were effective January 1, 2025. This increase will be effective on January 1, 2026 and will affect 71,871 Arizona policyholders (as of March 2025).

Cigna Healthcare of AZ:

Cigna estimates that 2,533 customers will be impacted by this rate increase. On average, customers will see an increase of 32.96%, excluding the impact of aging, with a range of increases from 16.87% to 42.64%. In addition to the factors described below, each customer’s rate increase depends on factors such as where they live and what plan they are enrolled in.

Ambetter/AZ Complete Health:

Arizona Complete Health (AZCH) currently provides health care coverage for over 112,000 members enrolled in our Ambetter plans. Premium rates are expected to increase on average by 49.0% for members on renewing plans, effective January 1, 2026. Annual rate changes may range between 36.8% and 57.1%, depending on what county current enrollees reside in and their current plan selection. Variations are primarily driven by underlying cost differences between different plan designs and regional cost trends. Note that these rate changes do not reflect any additional increases in a member’s calculated premium driven by aging an additional year at the point of renewal.

Imperial Insurance Companies, Inc:

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Oscar Health Plan Inc:

The purpose of this document is to present rate change justification for Oscar Health Plan, Inc. (Oscar’s) (HIOS ID 13877) Individual Affordable Care Act (ACA) products, with an effective date of January 1, 2026, and to comply with the requirements of Section 2794 of the Public Health Service Act as added by Section 1003 of the Patient Protection and Affordable Care Act (ACA).

Using in-force business as of March 2025 , the proposed average rate increase for renewing plans is 16.6%. Rate increases vary by plan due to a combination of factors including shifts in benefit leveraging and cost-sharing modifications. This rate increase is absent of rate changes due to attained age.

The rate increase impacts an estimated 10,102 members.

UnitedHealthcare:

Scope and Range of the Rate Increase

UHCAZ is filing 2026 rates for individual products. The proposed rate change is 43.67% and will affect 96,850 individuals. The rate changes vary between 41.29% and 53.76%. Given that the rate changes are based on the same single risk pool, the rate changes vary by plan due to plan design changes.

Financial Experience of the Product

The premium collected in plan year 2024 was $471,852,759. Incurred claims during this period were $309,930,841 and UHC expects payments of $91,732,612 for risk adjustment. The loss ratio, or portion of premium required to pay medical claims, for plan year 2024 is 81.53%.

As noted above, one carrier (Aetna/CVS/Banner) is dropping out of the individual market, while two others (Antidote and Imperial) have redacted their enrollment figures. This means I can't run a fully weighted average rate change and instead have to use estimated enrollees for those three.

Total 2025 Open Enrollment Period (OEP) on-exchange enrollment was ~423,000; assuming roughly another ~8,000 off-exchange enrollees (based on 2024 liability risk score data from CMS) gives a total of around ~431,200 individual market enrollees.

This leaves around ~138,000 exchange enrollees unaccounted for. If I assume equal enrollment in each of the 3 "blank" carriers, that means roughly 46,000 apiece, with the Aetna/CVS enrollees not being included in the weighted average at all.

This gives an estimated semi-weighted statewide average preliminary rate increase of 32.6%.

It's important to remember that this is for unsubsidized enrollees only; for subsidized enrollees, ACTUAL net rate hikes will likely be MUCH HIGHER for most enrollees due to the expiration of the improved ACA subsidies & the Trump CMS "Affordability & Integrity" rule changes.

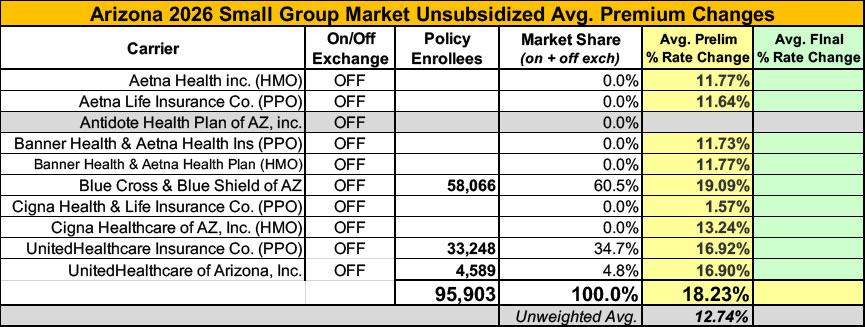

Meanwhile, I have no enrollment data at all for most of the small group carriers; the unweighted average 2026 rate hike there is around 12.7%.

| Attachment | Size |

|---|---|

| 1.34 MB | |

| 319.53 KB | |

| 81.22 KB | |

| 174.44 KB | |

| 259.52 KB | |

| 106 KB | |

| 153.49 KB |

Advertisement